Discounted Cash Flow (DCF) in Property Valuation: When to Use It and How It Works

EFEmile Frémont, MRICS — Lead Valuer, InterVal··6 min read

In short

Discounted cash flow (DCF) is an income-approach valuation method that forecasts a property's future cash flows and its exit (sale) value, then discounts each amount back to what it is worth today to arrive at a present value. It is the right method whenever a property's income is not flat and predictable — over- or under-rented properties, leases with breaks or expiries, and phased development.

Few valuation methods inspire as much quiet anxiety as discounted cash flow. Mention DCF and you can almost see practitioners brace: the sprawling spreadsheet, the discount rate pulled from thin air, the terminal value that somehow ends up driving the whole answer. Done badly, DCF is a black box that produces a confident number nobody can defend.

Done well, it is one of the most powerful tools a valuer has — the right method whenever a property's income is anything other than flat and predictable. This guide explains what DCF is, where it sits in the standards, when to reach for it instead of a simpler method, how it actually works step by step, and the inputs that make or break it.

What DCF is, in one idea

Discounted cash flow rests on a single principle: a pound received in five years is worth less than a pound today, because today's pound can be invested in the meantime. DCF makes that explicit. You forecast the cash flows a property will generate over a chosen period, plus the lump sum from selling it at the end, then "discount" each of those future amounts back to what they are worth today. Add them up and you have the present value — the most a rational investor should pay now to receive that future income stream.

It is the income approach taken to its logical, transparent conclusion: instead of capitalising a single year's income at one yield, you model the income year by year, with all its changes, and price the time and risk explicitly.

Where DCF sits in the standards

DCF is a method within the income approach, one of the three valuation approaches (market, income, cost). In the 2025 International Valuation Standards it relates to IVS 103 (Valuation Approaches and Methods), and because a DCF is itself a model, to IVS 105 (Valuation Models) — the standard, new for 2025, that holds valuers responsible for the integrity of the models they rely on. On the RICS side, the choice and justification of approach and method falls under VPS 3 of the Red Book. (For the full structure, see our practitioner guide to RICS Red Book compliance, and for how DCF relates to bases like Market Value and Investment Value, our guide to the bases of value.)

The standards point matters because IVS 105 makes the spreadsheet's output the valuer's responsibility. "The model said so" has never been a defence; since 2025 the standards say so in writing.

DCF vs. income capitalisation: when to use which

The income approach has two main methods, and choosing correctly is half the battle.

Income capitalisation (the "all-risks yield" approach) divides a single representative year's income by a market-derived yield. It is fast, well-evidenced, and entirely appropriate for a stabilised asset: a property let at market rent on standard terms with no looming events.

DCF earns its complexity when the income is not flat:

Over-rented or under-rented properties, where passing rent will step toward market rent at review or expiry;

Leases with breaks, expiries, voids or staged rent-free periods within the hold period;

Development and refurbishment, where cash flows are lumpy and phased;

Any situation where an investor's return depends on a specific business plan over time.

If you find yourself bending a single cap rate to account for events three years out, that is the method telling you to switch to DCF.

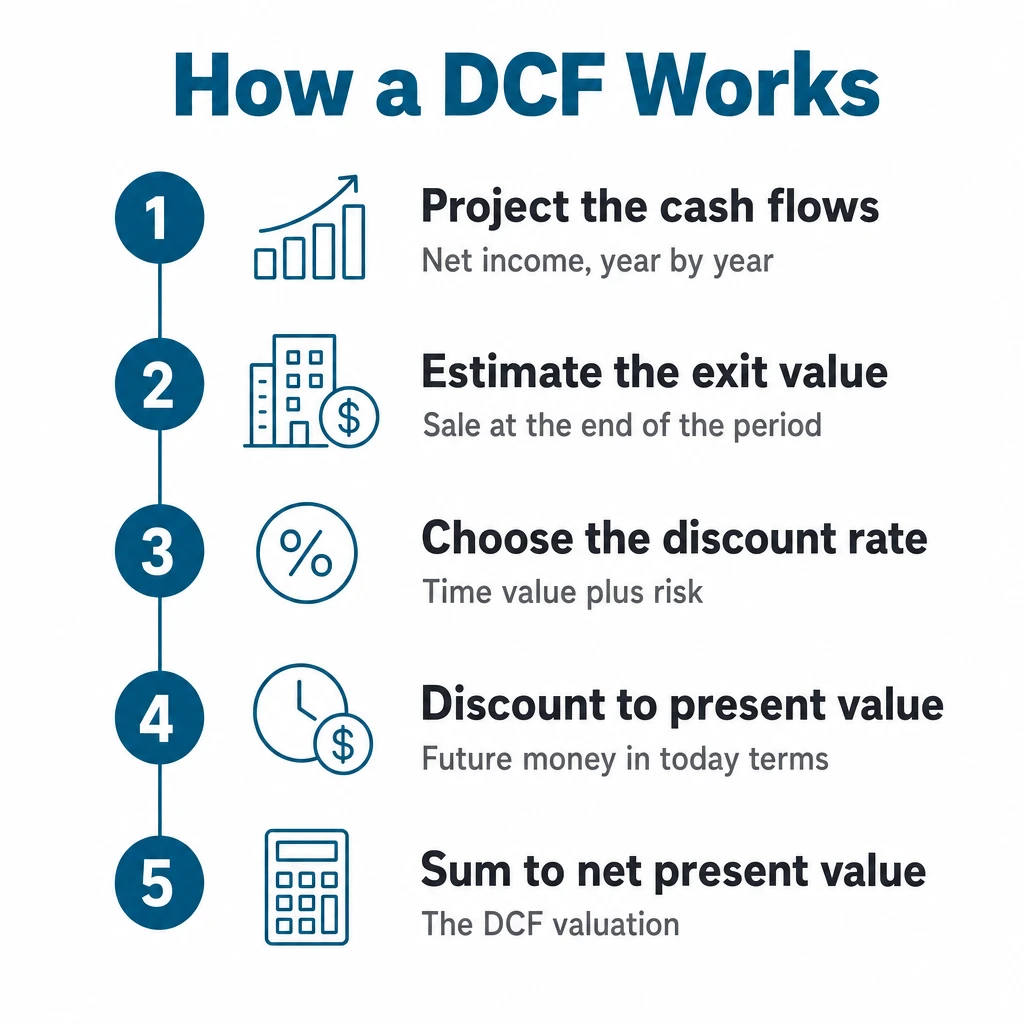

How a DCF works, step by step

A DCF in five steps — each one a deliberate, evidenced assumption, not a spreadsheet default.

Project the cash flows. Model the net income for each year of an explicit forecast period (commonly 5 or 10 years) — rent in, deducting voids, non-recoverable costs, capital expenditure and the like — reflecting reviews, expiries and lettings as they fall.

Estimate the exit (terminal) value. Assume a sale at the end of the period, usually by capitalising the following year's income at an exit yield. This single figure often represents a large share of the total value, so it deserves real scrutiny — not a copied assumption.

Choose the discount rate. The rate that converts future money to present value, reflecting the time value of money plus the risk of this specific cash flow. It is the input valuers agonise over most, and rightly so.

Discount each amount to present value. Apply the discount rate to every yearly cash flow and to the exit value, so each is expressed in today's money.

Sum to the net present value. Add the discounted cash flows and discounted exit value. The total is the DCF valuation — the present value of the whole future stream.

The inputs that make or break it

A DCF is only ever as good as its assumptions, and three inputs carry most of the weight:

The discount rate. Small changes move the answer a lot. It must be reasoned from market evidence and the asset's risk, and the reasoning must be on the file — not reverse-engineered to hit a target number.

Rental growth and market assumptions. Optimistic growth compounds quietly over a ten-year model and can flatter a value into meaninglessness. Conservative, evidenced assumptions age far better.

The exit yield. Because the terminal value is so large a component, a small shift in exit yield can swing the result more than years of income detail.

This is why sensitivity testing is not optional good practice but core to a credible DCF: show how the value moves as the discount rate, growth and exit yield vary, so the client sees the range and the key drivers rather than a single false-precise figure.

Where DCF goes wrong

Most DCF failures are not conceptual — they are mechanical, and they almost always live in the spreadsheet:

A dragged formula that skips a year, or a hard-coded cell where a reference belonged;

A terminal value quietly dominating the answer while attention goes to the income detail;

Assumptions buried in cells with no record of where they came from — so the file cannot show the reasoning a reviewer will ask for;

No sensitivity analysis, presenting a single number as if it were certain.

These are the same structural weaknesses we covered in valuation software vs. spreadsheets — and in a DCF, where the answer is so sensitive to a handful of inputs, they bite hardest.

The discipline of DCF is in the assumptions and the audit trail, not the arithmetic.

Where software fits

DCF is the strongest argument for doing valuation in a structured platform rather than a hand-built spreadsheet. The calculation should be reliable by construction; the assumptions should be captured as structured inputs, not loose cells; sensitivity testing should be a button, not a manual rebuild; and every assumption should land in the audit trail so the reasoning survives. InterVal brings discounted cash flow into the guided workflow — with the Professional plan — alongside the market and income-capitalisation methods, so the model's integrity and its record are part of the process, exactly as IVS 105 now expects.

The bottom line

DCF is not a black box and it is not only for financial analysts. It is the right method whenever a property's income changes over time — and most institutional and many commercial assets do. The skill is not in the discounting arithmetic, which never changes; it is in choosing evidenced assumptions, stating them clearly, testing their sensitivity, and keeping a record that lets the valuation stand up later. Get that discipline right and DCF stops being the method valuers dread and becomes the one that answers the questions a single yield never could.

This guide is provided for general information and reflects the standards in force at the date of publication. It summarises methodology; always refer to the current editions of the International Valuation Standards and RICS Valuation – Global Standards, and to guidance applicable in your jurisdiction.

Frequently asked questions

When should you use DCF instead of income capitalisation?

Use income capitalisation for a stabilised asset — let at market rent on standard terms with no looming events. Reach for DCF when the income changes over time: over- or under-rented properties, leases with breaks, expiries or voids, phased development, or any case where the return depends on a business plan over time. If you are bending a single cap rate to account for events years out, that is the method telling you to switch.

What are the key inputs in a DCF valuation?

Three inputs carry most of the weight: the discount rate (small changes move the answer a lot), rental growth and market assumptions (optimism compounds quietly over ten years), and the exit yield (the terminal value is often a large share of the total). Because the result is so sensitive to these, sensitivity testing is core to a credible DCF, not optional.

What are the five steps of a DCF valuation?

1) Project the net cash flows for each year of an explicit forecast period; 2) estimate the exit (terminal) value, usually by capitalising the following year's income at an exit yield; 3) choose the discount rate; 4) discount each yearly cash flow and the exit value to present value; 5) sum them to the net present value — the DCF valuation.

Where does DCF sit in the RICS Red Book and IVS?

DCF is a method within the income approach. In IVS 2025 it relates to IVS 103 (Valuation Approaches and Methods) and, because a DCF is itself a model, to IVS 105 (Valuation Models). On the RICS side, the choice and justification of approach and method falls under VPS 3 of the Red Book.

Why is DCF often called a 'black box'?

Because the answer is so sensitive to a handful of inputs, a badly built DCF can produce a confident number nobody can defend. Most failures are mechanical — a dragged formula skipping a year, a terminal value quietly dominating the result, assumptions buried in cells with no record, or no sensitivity analysis. Evidenced assumptions, sensitivity testing and an audit trail are what turn a black box into a defensible valuation.

An audit trail sounds like bureaucracy; it is the opposite — the record of how a valuation was reached, and the only thing that lets a reviewer, insurer or regulator rely on it years later. What a defensible audit trail contains, where the RICS Red Book and IVS require it, why files fail without one, and why it should be captured as you work rather than reconstructed from memory.

Valuation files are some of the most sensitive data a professional handles — so is the cloud safe for them? A practical framework from InterVal's technology lead: what real cloud security looks like (encryption, access control, audited hosting, data residency, backups, audit trail, data ownership), the questions to ask any vendor, and why the real risk is usually the laptop-and-email workflow, not the cloud.

Subscribe to our Newsletter

Subscribe to our newsletter to receive exclusive offers, latest news and updates.

Less than one hour to obtain a fully standard Compliant Valuation.