Bases of Value Explained: Market Value, Fair Value, Investment Value and the Rest

EFEmile Frémont, MRICS — Lead Valuer, InterVal··6 min read

In short

A basis of value defines what a valuation figure actually means — worth to whom, and for what purpose. The International Valuation Standards (IVS 102, 2025) recognise six: Market Value, Market Rent, Investment Value, Equitable Value, Synergistic Value and Liquidation Value. The same property can carry several entirely correct values on the same day, depending on which basis you measure.

Ask a non-valuer what a property is "worth" and they expect a single number. Ask a valuer, and the honest first answer is a question: worth to whom, and for what purpose? The same building can carry several entirely different, entirely correct values on the same day — depending on which basis of value you are measuring.

Choosing the right basis is not a technicality. It is the most consequential decision in a valuation, because it defines what the number actually means. Use Market Value where Investment Value was needed, and the figure is precise, defensible, and wrong for the client's purpose. This guide explains each basis defined in the International Valuation Standards, when to use it, and the one naming confusion that trips up even experienced practitioners.

Where "bases of value" live in the standards

Bases of value are governed by the International Valuation Standards (IVS). In the 2025 edition, effective 31 January 2025, they sit in IVS 102 — note that this moved from IVS 104 in the previous edition, so older references and templates may cite the wrong chapter. On the RICS side, the requirement to select and clearly state the basis of value lives in VPS 2 of the Red Book. (For the full picture of how the Red Book is structured, see our practitioner guide to RICS Red Book compliance.)

The standards do two things here. They define a set of recognised bases so that "Market Value" means the same thing to a valuer in Singapore and a lender in London. And they require you to state, explicitly and in advance, which basis you are using — because a number without its basis is ambiguous at best and misleading at worst.

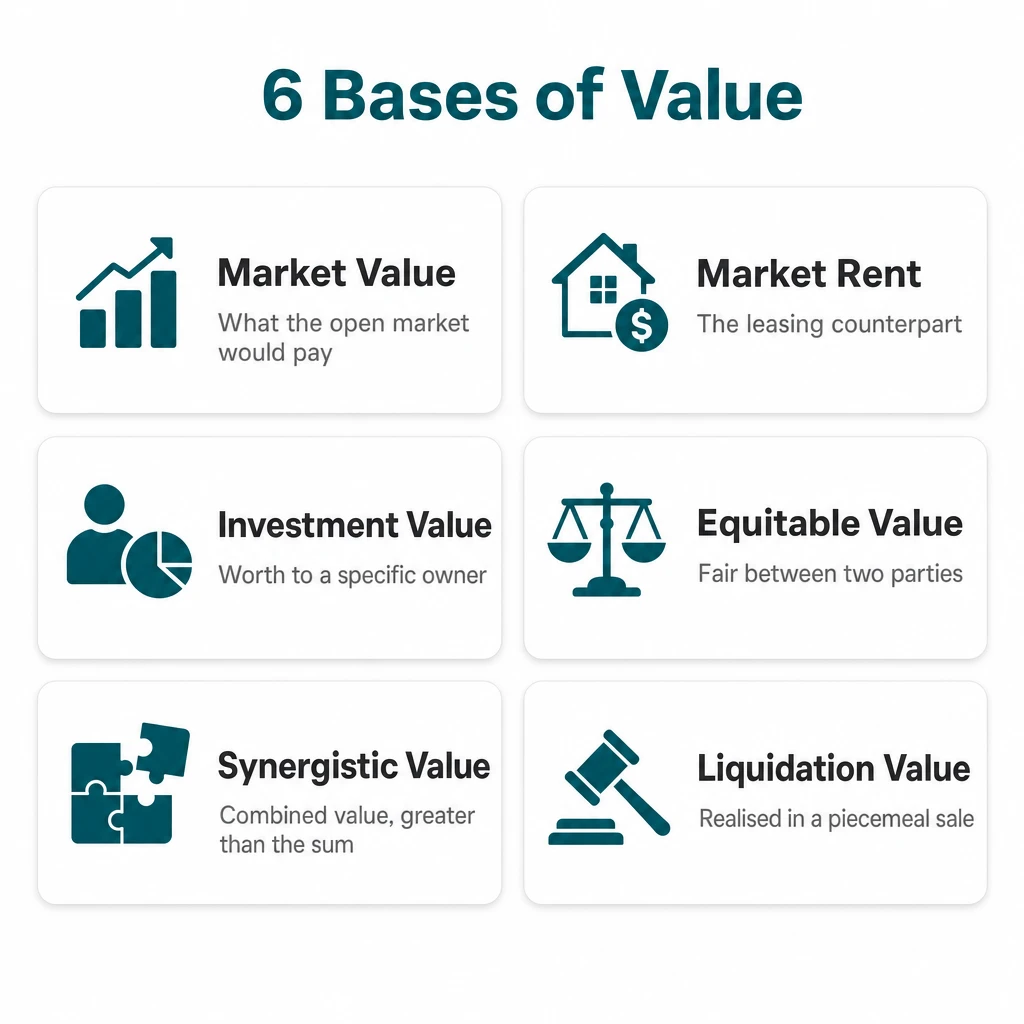

The IVS-defined bases of value

Market Value

The default basis for most real-property valuations. IVS defines Market Value as the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction, after proper marketing, where the parties each acted knowledgeably, prudently and without compulsion.

Every phrase carries weight: willing (neither forced), arm's-length (unconnected parties), proper marketing (adequate exposure to the market), without compulsion (no special urgency). Market Value is what most clients mean by "what's it worth" — a hypothetical, market-derived figure independent of any particular buyer.

Market Rent

The leasing counterpart of Market Value. It is the estimated amount for which an interest in property should be leased on the valuation date between a willing lessor and willing lessee on appropriate lease terms, in an arm's-length transaction after proper marketing. The lease terms matter enormously — Market Rent on a full-repairing-and-insuring lease is not the same number as Market Rent on a lease with different obligations, which is why the assumed terms must be stated.

Investment Value (or Worth)

The value of an asset to a particular owner or prospective owner, for their individual investment or operational objectives. Unlike Market Value, it is entity-specific: it reflects that buyer's own cost of capital, tax position, portfolio synergies, or strategic plans. Investment Value is the right basis when the question is "what is this worth to me?" — for an acquisition decision, for example — rather than "what would the market pay?" The two can diverge sharply, and that gap is often exactly the information a client needs.

Equitable Value

The estimated price for transferring an asset between two specific, identified parties that reflects the respective interests of those parties. It is broader than Market Value: it considers what is fair between these two particular parties, who may not be the hypothetical willing buyer and seller of the open market. Equitable Value is common where there is no open-market exposure — a transfer between related companies, or a buy-out between shareholders.

Synergistic Value

Sometimes called marriage value or merger value. It is the additional value created when two or more assets or interests combine to produce a value greater than the sum of the separate values. The classic example: two adjoining plots, each modestly valuable alone, that together enable a development neither could support individually. The synergy belongs to the combination, so the basis has to be stated carefully — it is not what either party would achieve on its own.

Liquidation Value

The amount realisable when assets are sold on a piecemeal basis, reflecting the costs of getting them into saleable condition and the costs of disposal. It can be assessed under an orderly liquidation (a reasonable marketing period) or a forced sale (compressed timescale, often well below Market Value). A forced sale, strictly, is a circumstance rather than a basis — the standards are clear that "forced sale value" is not a basis of value in itself, but Market Value or Liquidation Value assessed under the special assumption of a forced disposal.

The Fair Value trap

"Fair Value" is where even seasoned valuers get caught, because the term means two different things depending on the context.

IFRS Fair Value is an accounting concept (IFRS 13): the price to sell an asset or transfer a liability in an orderly transaction between market participants at the measurement date. In most real-property cases it is broadly consistent with Market Value.

Equitable Value is what older editions of IVS used to call "Fair Value" — the between-two-specific-parties basis described above. IVS deliberately renamed it to Equitable Value precisely to stop the confusion with the IFRS term.

If a client asks for "fair value," the single most useful thing you can do is ask which one they mean. The answer changes the basis, the definition, and potentially the figure.

Quick reference: which basis, when

The six IVS-defined bases of value, and the question each one answers.

The pattern to notice: Market Value and Market Rent ask "what would the open market do?"; Investment Value asks "what is it worth to this specific party?"; Equitable Value asks "what is fair between these two parties?"; Synergistic Value asks "what does the combination create?"; and Liquidation Value asks "what could be realised if we had to sell now?" Same asset, six legitimate questions, six different answers.

Why stating the basis explicitly is a compliance issue

The Red Book does not leave the basis of value to inference. VPS 2 requires it to be appropriate to the purpose, explicitly identified, and properly defined in the terms of engagement and the report. This is not bureaucracy — it is what makes the figure usable. A lender, a court, or an auditor reading your report needs to know whether they are looking at an open-market figure or a worth-to-a-specific-party figure, because they will rely on it very differently.

This is also where a spreadsheet-and-Word workflow quietly fails: nothing in a blank template prompts you to confirm that the stated basis matches the purpose, or carries that basis consistently through to the report. (We wrote about that gap in valuation software vs. spreadsheets.) In InterVal, the basis of value is a structured field captured up front and carried through the assignment, so the report cannot drift from the engagement. You can see how that reads in the finished documents in our sample reports.

The first question on any assignment is not "how much?" but "on what basis?"

The bottom line

"What's it worth?" has no single answer until you fix the basis of value. Market Value, Market Rent, Investment Value, Equitable Value, Synergistic Value and Liquidation Value are not interchangeable synonyms — each answers a different question, and the standards exist so that everyone reading your report knows exactly which question you answered. Get the basis right, state it explicitly, and the rest of the valuation has firm ground to stand on. Get it wrong, and a perfectly executed valuation can still be the wrong tool for the client's job.

This guide is provided for general information and reflects the standards in force at the date of publication. Definitions are summarised; always refer to the current edition of the International Valuation Standards and RICS Valuation – Global Standards for the authoritative wording, and to guidance applicable in your jurisdiction.

Frequently asked questions

What are the IVS bases of value?

Six: Market Value (open-market exchange between willing parties), Market Rent (its leasing counterpart), Investment Value or Worth (value to a particular owner), Equitable Value (a fair price between two specific identified parties), Synergistic Value (the extra value when assets combine), and Liquidation Value (what is realisable in a piecemeal sale).

What is the difference between Market Value and Investment Value?

Market Value is a hypothetical, market-derived figure independent of any particular buyer — what the open market would pay. Investment Value is entity-specific: the worth of the asset to a particular owner given their cost of capital, tax position, portfolio synergies or strategic plans. The two can diverge sharply, and that gap is often exactly what the client needs to know.

Is Fair Value the same as Market Value?

It depends which Fair Value is meant. IFRS Fair Value (IFRS 13) is an accounting concept broadly consistent with Market Value in most property cases. But older editions of IVS used 'Fair Value' for what is now called Equitable Value — the between-two-specific-parties basis. If a client asks for 'fair value', ask which one they mean, because the answer changes the basis, the definition and potentially the figure.

Is 'forced sale value' a basis of value?

No. A forced sale is a circumstance, not a basis. The standards are clear that 'forced sale value' is not a basis in itself — it is Market Value or Liquidation Value assessed under the special assumption of a forced disposal within a compressed timescale.

Where are bases of value defined in the standards?

In IVS 102 (2025 edition, effective 31 January 2025) — note this moved from IVS 104 in the previous edition. On the RICS side, VPS 2 of the Red Book requires the basis of value to be appropriate to the purpose, explicitly identified and properly defined.

An audit trail sounds like bureaucracy; it is the opposite — the record of how a valuation was reached, and the only thing that lets a reviewer, insurer or regulator rely on it years later. What a defensible audit trail contains, where the RICS Red Book and IVS require it, why files fail without one, and why it should be captured as you work rather than reconstructed from memory.

Valuation files are some of the most sensitive data a professional handles — so is the cloud safe for them? A practical framework from InterVal's technology lead: what real cloud security looks like (encryption, access control, audited hosting, data residency, backups, audit trail, data ownership), the questions to ask any vendor, and why the real risk is usually the laptop-and-email workflow, not the cloud.

Subscribe to our Newsletter

Subscribe to our newsletter to receive exclusive offers, latest news and updates.

Less than one hour to obtain a fully standard Compliant Valuation.