Valuation Software vs. Spreadsheets: When Excel and Word Stop Being Enough

JBJoachim Bertot, Founder, InterVal··6 min read

In short

Spreadsheets and Word templates can produce a good valuation report, but they put the entire burden of compliance on human memory: version chaos, silent formula errors, compliance drift as standards change, no audit trail, and collaboration friction. A structured valuation platform makes the process itself carry the standards, the required documents and the audit trail — so compliance is built in rather than reconstructed at the end.

Walk into almost any valuation practice and you will find the same toolkit behind even the most sophisticated reports: a Word template that has been copied and re-copied for years, a folder of Excel sheets with hand-built formulas, and an inbox full of comparable evidence. It works. Valuers have produced perfectly good reports this way for decades.

So why change?

I ask because I lived the answer. In 2018, my firm — then the only RICS-accredited valuation practice in Mongolia — was asked by the International Monetary Fund to review the valuation reports behind real estate held as collateral across the country's banks. Thousands of files. The overwhelming majority failed to follow RICS, IVS, or any standard at all. Almost none of those failures were about valuation judgement. They were about process: missing terms of engagement, undefined bases of value, no record of the inspection, formulas no one could reconstruct. The spreadsheet had quietly let every one of them through.

This article is an honest look at where the spreadsheet-and-Word workflow costs you, where it is genuinely fine, and what a purpose-built platform changes.

The workflow most valuers still run

The typical assignment looks something like this. You copy last month's Word report and start deleting the parts that don't apply. You open a fresh Excel sheet — or duplicate an old one — to run the comparables and the calculations. Inspection notes live in a notebook or a phone. Evidence sits in an email thread. At the end, you reconcile it all by hand, export a PDF, and hope nothing was left from the file you copied.

It is flexible, familiar, and free at the point of use. Those are real advantages, and they are exactly why the workflow persists. But the flexibility hides a set of recurring costs that only show up when something goes wrong — an audit, a challenge, a complaint, a new hire trying to follow your file.

Where the spreadsheet workflow breaks

1. Version chaos

"Valuation_final_v3_REALLY_final.xlsx" is a joke because it is true. Without a single source of truth, every assignment spawns copies, and the wrong copy gets sent more often than anyone admits. A figure corrected in one file lives on, uncorrected, in three others.

2. Silent formula errors

A spreadsheet will happily calculate the wrong answer with total confidence. A dragged formula that skips a row, a hard-coded number where a reference should be, a rounding rule applied inconsistently — none of these announce themselves. Research into spreadsheet error rates has consistently found that a large share of business-critical spreadsheets contain mistakes. In a valuation, that error is the deliverable.

3. Compliance drift

Standards change. The RICS Red Book was restructured in 2025, moving from five mandatory Valuation Practice Statements to six and renumbering several of them. Every Word template still citing the old structure is now subtly non-compliant — and a copied template propagates that error across every future report until someone notices. A spreadsheet has no idea what the Red Book requires. It cannot prompt you for terms of engagement, flag a missing basis of value, or remind you that a draft statement is needed. (If you want the full picture of what the standards now require, our practitioner guide to RICS Red Book compliance walks through it stage by stage.)

4. No audit trail

This is the one that hurt most during the IMF review. Compliance is not what you did; it is what you can show you did, years later, to a reviewer who was not there. A spreadsheet records the final number, not the reasoning, the evidence, the assumptions agreed with the client, or the order things happened in. When a file is challenged, "trust me, I did it properly" is not a defence.

5. Collaboration friction

The moment two people touch the same assignment, the spreadsheet workflow strains. Files get emailed back and forth, changes overwrite each other, and the senior valuer reviewing the work has no way to see what the junior actually changed. Scale it to a team valuing a portfolio and the coordination cost becomes the bottleneck.

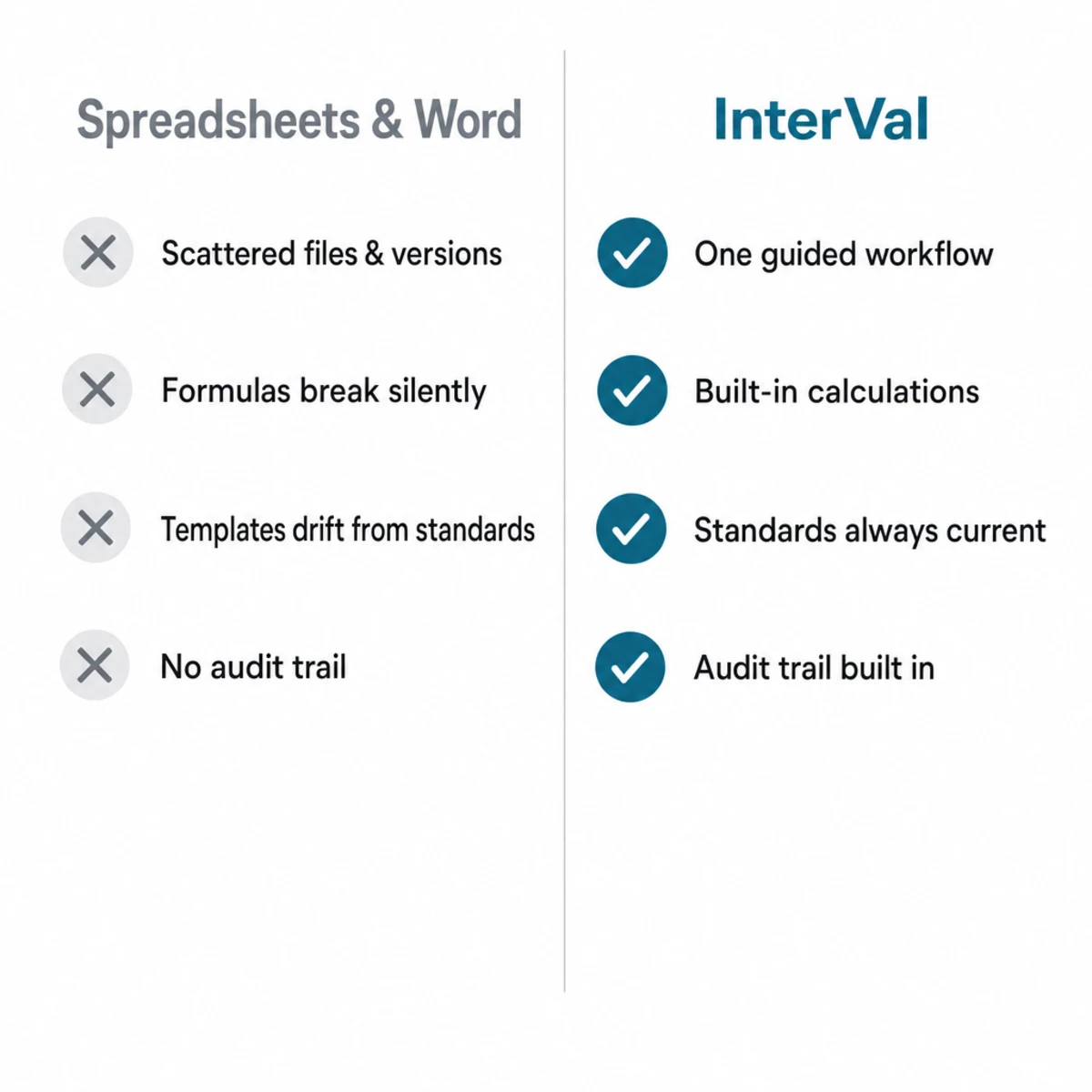

Spreadsheet workflow vs. a structured valuation platform

Here is the same work, side by side.

The same assignment, two workflows: scattered and manual versus structured and standards-aware.

The difference is not that one is "digital" and the other is not — a spreadsheet is digital. The difference is that a structured platform makes the process the product. The standards, the required documents, and the audit trail are built into how you work, instead of depending on your memory and discipline at the end of every job.

What actually changes with a purpose-built platform

In InterVal, a valuation is a guided workflow rather than a blank template. The platform walks an assignment from conflict-of-interest checks and terms of engagement, through inspection and method selection, to the final report — generating the documents from consistent templates and building the audit trail as you go. Concretely, that means:

One source of truth. No copies, no "which version is current" — the assignment is the file.

Standards built in. The workflow follows the current RICS Red Book and IVS structure, so the required steps and documents are present by construction, not by recollection.

Calculations you don't hand-build. Market approach and income capitalisation are handled inside the platform (with DRC and DCF arriving in the Professional plan), so there are no dragged formulas to break.

An audit trail that writes itself. Engagement, evidence, assumptions, drafts and the final report are connected — the thing a reviewer, insurer or regulator can actually verify.

Real collaboration. Teams work on the same assignment in real time, with reports generated from shared templates instead of emailed spreadsheets.

You can see what the output looks like in our sample reports, each mapped to the documents the Red Book expects.

When the process carries the compliance, the valuer is free to focus on judgement.

When a spreadsheet is genuinely fine

I am not going to pretend software is always the answer. If you do a handful of valuations a year, work entirely alone, and never face an audit or a compliance review, a well-built spreadsheet and a careful Word template can serve you well. The cost of the status quo is low when volume is low and you are the only person who ever touches the file.

The calculus changes the moment any of these is true: you are producing valuations at volume, you work in a team, your reports go to lenders or courts, or you are a RICS member whose files can be monitored under Valuer Registration. At that point the spreadsheet stops being free — it is just deferring a cost to the worst possible moment, when a file is challenged and the evidence isn't there.

The honest bottom line

The spreadsheet didn't fail those Mongolian banks because valuers were careless. It failed because the tool put the entire burden of compliance on human memory and discipline, every single time, with no safety net. That is a structural problem, and structure is exactly what software can provide.

Whether you systematise with a platform or with rigorous internal procedure, the principle is the same: compliance and consistency should be properties of your process, not a heroic effort at the end of each assignment. The question is not whether your spreadsheet can produce a good report — it can. The question is whether it can prove, two years from now, that it did.

This article reflects general industry experience and the standards in force at the date of publication. Always refer to the current edition of RICS Valuation – Global Standards and to RICS guidance applicable in your jurisdiction.

Frequently asked questions

Why do so many valuers still use spreadsheets and Word?

Because the workflow is flexible, familiar and free at the point of use — real advantages that explain why it persists. The catch is that the flexibility hides recurring costs that only surface when something goes wrong: an audit, a challenge, a complaint, or a new hire trying to follow the file.

What are the risks of using spreadsheets for property valuation?

Five recurring ones: version chaos (no single source of truth), silent formula errors that calculate the wrong answer with total confidence, compliance drift as templates fall behind changing standards, no audit trail (the sheet records the final number, not the reasoning), and collaboration friction the moment two people touch the same file.

When is a spreadsheet good enough for valuations?

If you do a handful of valuations a year, work entirely alone, and never face an audit or compliance review, a well-built spreadsheet and careful Word template can serve you well. The calculus changes the moment you work at volume, in a team, for lenders or courts, or as a RICS member whose files can be monitored under Valuer Registration.

What does a valuation platform do that a spreadsheet cannot?

It makes the process the product: one source of truth instead of copied files, the current RICS Red Book and IVS structure built in, calculations you don't hand-build, an audit trail that writes itself as you work, and real-time collaboration. The standards and required documents are present by construction, not by recollection at the end of each job.

An audit trail sounds like bureaucracy; it is the opposite — the record of how a valuation was reached, and the only thing that lets a reviewer, insurer or regulator rely on it years later. What a defensible audit trail contains, where the RICS Red Book and IVS require it, why files fail without one, and why it should be captured as you work rather than reconstructed from memory.

Valuation files are some of the most sensitive data a professional handles — so is the cloud safe for them? A practical framework from InterVal's technology lead: what real cloud security looks like (encryption, access control, audited hosting, data residency, backups, audit trail, data ownership), the questions to ask any vendor, and why the real risk is usually the laptop-and-email workflow, not the cloud.

Subscribe to our Newsletter

Subscribe to our newsletter to receive exclusive offers, latest news and updates.

Less than one hour to obtain a fully standard Compliant Valuation.